Two markets, two signals

Resale supply is constrained. New housing demand is easing. The gap between the two is where the story sits.

A few weeks back I explored the idea that planning approvals are routinely blamed for Australia’s housing shortage - yet when we dug into the numbers, the story proved far more nuanced.

Revisit

A Moment with Mike

The Long Read is behind the paywall and also housed here:

This post I want to explore the interplay between housing supply and demand and to see what an update of the national charts tell us about the current state of play.

Before refreshing the data, my gut feel was that the “permanent shortage” narrative - particularly for owner-occupier new housing - might be starting to wear a little thin.

This time I’m revisiting the national market through two lenses: the established market and the new housing market.

Same country. Same economy. Two very different signals.

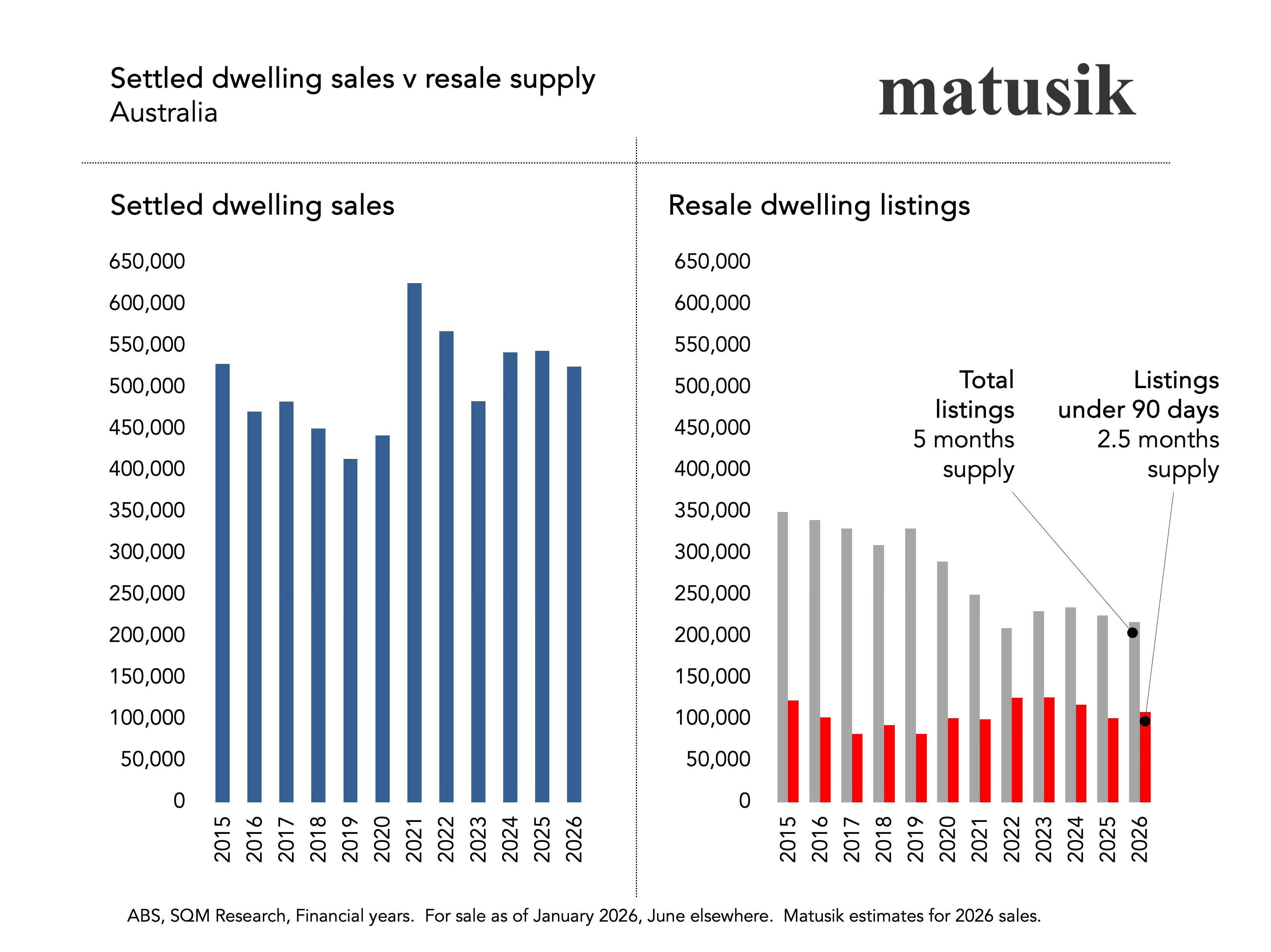

1. The established market: sales versus listings

Start with turnover.

Settled dwelling sales remain elevated. Even allowing for some easing as higher interest rates bite and price growth moderates, turnover is still running well above the softer pre-pandemic years.

Now compare that to resale supply.

Total listings nationally equate to roughly five months of supply. Listings under 90 days - the stock that really matters for price discovery - sit closer to 2½ months. That is tight by any historical measure.

So we have a simple imbalance: sales are relatively high; resale supply is relatively low.

Could sales soften from here? Yes. Rising mortgage rates, stretched borrowing capacity and more modest capital growth expectations will temper some marginal demand.

But resale supply is the bigger story.

Why has resale tightened and why might it remain so?

First, the mortgage lock-in effect. A large cohort refinanced or purchased at ultra-low fixed rates. Even though many of those loans have rolled, the replacement rate is still materially higher than what borrowers paid during 2020–2022. Trading up means resetting the entire debt stack at today’s pricing. Many households are choosing to stay put.

Second, demographics. Baby Boomers are not listing in the numbers many expected. They are wealth-rich, often debt-light and increasingly ageing in place. The family home is not just shelter; it is optionality, security and in many cases a tax-effective asset.

Third, transaction costs. Stamp duty remains a formidable friction. When the cost to move can run into six figures in Sydney or Melbourne, inertia becomes rational.

Fourth, replacement risk. Even if you sell, what do you buy? In many sub-markets choice remains limited.

Fifth, the investment equation. Rents have surged and vacancy is stuck between 1% and 1.5% nationally. For many landlords, the income case to hold has improved relative to selling, particularly if capital gains tax would crystallise on exit.

Add those together and resale supply does not look like it is about to flood the market.

This is why established prices have proven resilient. Not because demand is unbounded, but because supply remains constrained.

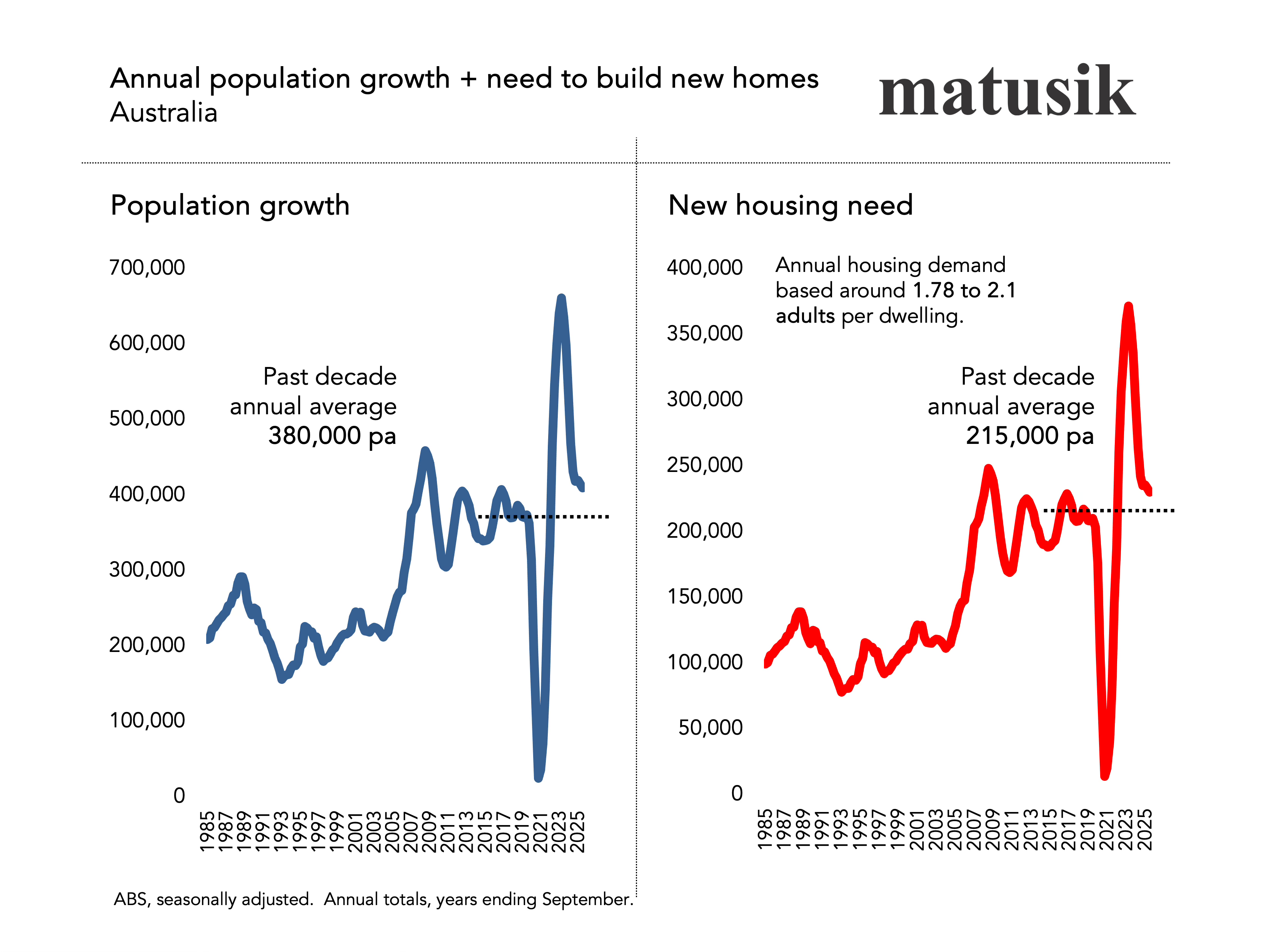

2. The new housing market: population and underlying demand

Now flip to new housing.

Underlying demand is best measured by population growth adjusted for the number of adults per dwelling. Statistically, and since 1985, Australia has averaged about 1.78 to 2.1 adults per dwelling depending on proportion of children in the population growth mix. Regardless, when population surges, the need to build surges.

Over the past decade, annual population growth averaged about 380,000. In the immediate post-pandemic rebound, it spiked dramatically, pushing annual new housing demand well above 300,000 dwellings.

That spike drove the “chronic undersupply” narrative. And to be fair, it was real. Completions could not keep pace with the migration surge, construction costs exploded and projects stalled.

But population growth is now falling back toward trend.

As it does, new housing demand also eases.

The past decade’s average need sat around 215,000 dwellings per annum. Recent demand has been higher, but as migration normalises, the arithmetic shifts.

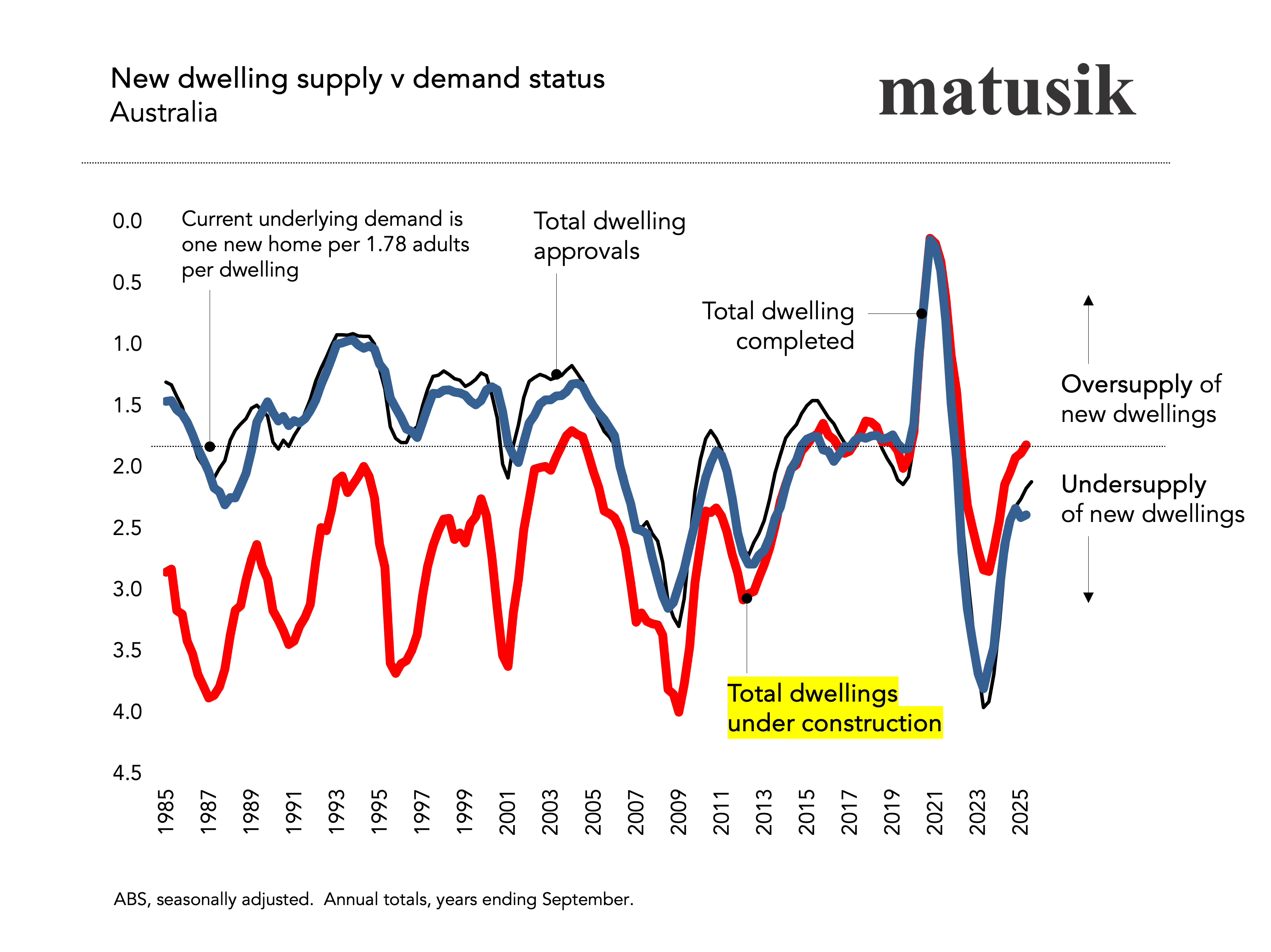

Undersupplied?

But when you overlay dwelling approvals, completions and the pipeline under construction, something interesting emerges.

We are no longer in the depths of acute undersupply.

My chart suggests we are moving toward balance.

The backlog of dwellings under construction - swelled during the HomeBuilder and migration surge period - is progressively completing. Approvals have softened, yes, but so too has underlying demand.

Meanwhile rental vacancy remains extremely tight. That tells us that new investment supply is still lagging. Investor lending has not recovered sufficiently to rebuild rental stock at the pace required.

But for owner-occupiers seeking a new dwelling - particularly detached housing in growth corridors - the story is changing.

The chronic undersupply that dominated headlines since 2021 may be closer to its end than many think.

This is not a case for oversupply. We are nowhere near that. It is a reminder that housing markets move in gradients, not headlines.

End note

Established housing remains tight because resale supply is constrained.

New housing demand is easing because population growth is normalising.

The interaction of those two forces matters.

If resale listings stay thin while new supply catches up to a moderating demand profile, we could see a period where price growth flattens rather than surges, not because of collapse, but because balance is restored.

That challenges the prevailing narrative.

Housing markets are not defined by slogans. They are defined by flows - of people, credit and stock.

Right now, the flows suggest the established market is tight.

The new market? It may be quietly rebalancing. Well at least for owner residents.

And if that is true and if this trend continues then the next chapter in Australia’s housing story will look very different from the one we have been telling ourselves since the pandemic.