Press reset

Housing speculation is not an economic strategy

A morning post today, as I am sure most of you will have better things to do from this afternoon.

Last month I posted a Missive titled Sugar Hit. It struck a nerve.

The piece sparked plenty of debate, both publicly and privately. Some agreed. Some strongly did not. A few were particularly animated.

Rather than reply in fragments across socials and DMs, I thought it better to respond properly.

Revisit

Debt

For much of the past 25 years, economic growth and government spending largely moved together. But from about 15 years ago they haven’t.

GDP has grown at roughly 2.5% a year. Government spending - state and federal combined - has tracked a tad over 3%. On the surface, that gap looks minor. Over time, it isn’t. It compounds. And what it leaves behind are structural deficits baked into the system.

The most obvious consequence is the interest bill.

Australia now spends about $50 billion a year just servicing government debt. That’s more than we spend on aged care. It’s equivalent to rebuilding the Bruce Highway or other similar big infrastructure projects multiple times over. And it is money committed before a single service is delivered.

Even on Treasury’s relatively optimistic projections, public debt could rise by as much as 200% within the next two decades. So our debt levels could triple in size within a generation.

Yes, we are not alone. Debt levels in the US, Japan and much of Europe already exceed the size of their economies. By comparison, Australia is expected to sit closer to 40% of GDP by the end of the decade.

But being better positioned is not the same as being immune. Especially when, at the same time, we have steadily eroded our own self-reliance. In a more uncertain world, that looks less like strategy and more like complacency.

Moreover, once higher debt and interest costs take hold, they are difficult to unwind - especially as ageing populations demand more from public balance sheets.

The lesson from elsewhere is simple: delay reduces choice.

Australia is running out of easy options. Waste, duplication and poor prioritisation are no longer harmless inefficiencies. They are costs we carry forward.

In a more volatile world, every dollar misspent today is one we won’t have when it counts.

Maybe we really should start paying the piper!

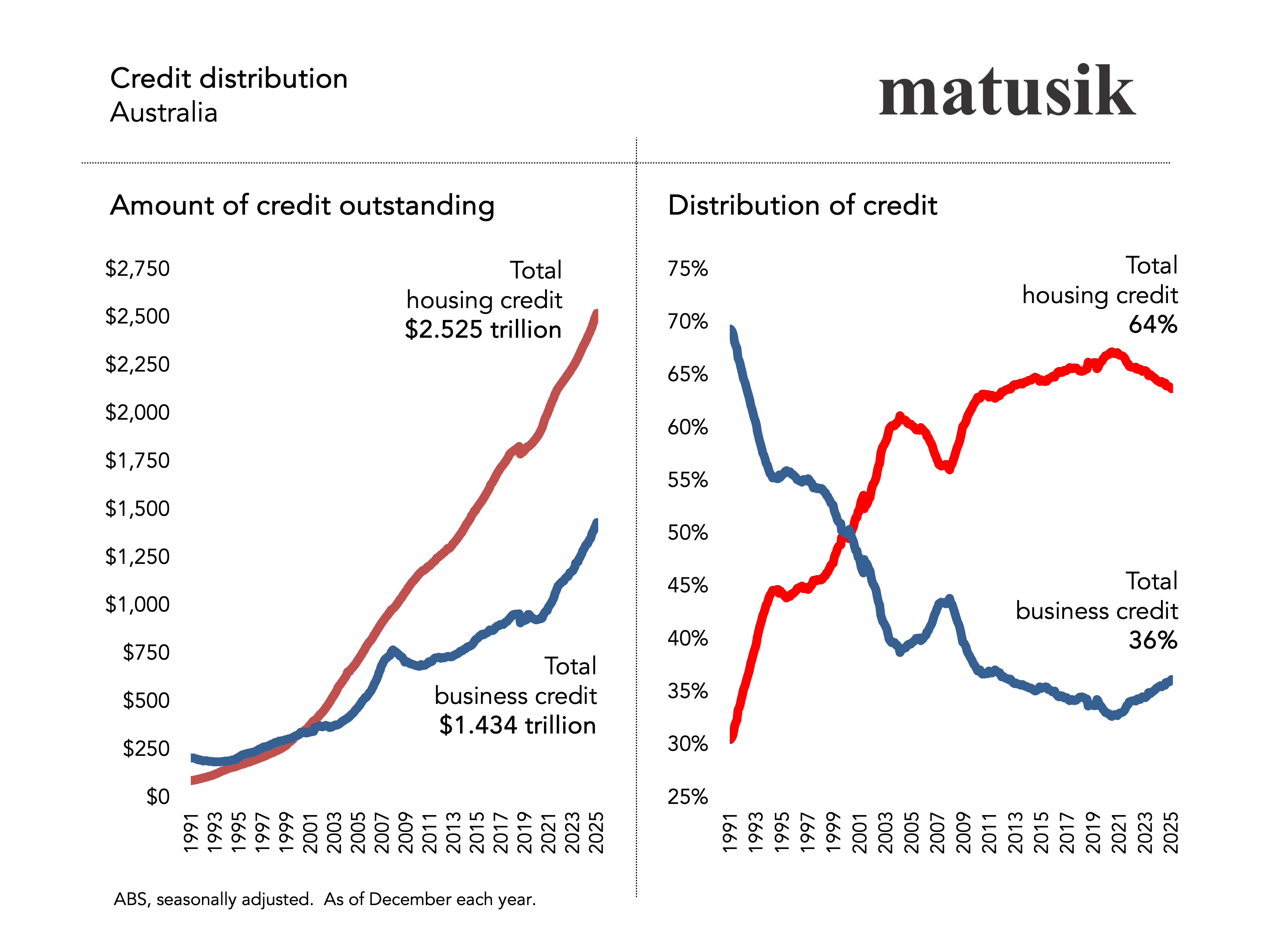

Credit

If you want a quick graphic that explains modern Australia - for mine - it is the credit distribution charts below.

In the early 1990s, roughly half of domestic credit flowed to business and just over a third to housing. Today, more than 60% flows to housing and just over 30% to business.

That is not cyclical. It is structural.

Household debt - not government debt like discussed above but the personal/business debt that we own directly to the bank or its equivalent - has climbed from roughly 40% of GDP in the mid 1990s to around 110% today.

Australia now sits alongside Canada, New Zealand and again parts of Northern Europe as one of the most leveraged household sectors in the developed world.

High household debt is not inherently reckless. These - including Australia - are wealthy, institutionally stable countries with strong banking systems. But structure matters.

When mortgages dominate bank balance sheets, the economy becomes heavily exposed to property values and housing turnover. When housing credit expands, activity expands. When it slows, the economy feels it.

Business credit, meanwhile, has steadily declined as a share of lending over three decades.

The direction of credit tells you a lot about an economy. When it chases existing land, prices rise but little else changes. When it backs enterprise, it builds capacity - more capital, higher wages and better productivity over time.

Australia has increasingly chosen the former.

It’s time to switch sides!

Press reset

If the rebuilt federal Liberal Party of Australia is serious about economic credibility, the path is clear - but not easy.

It isn’t about culture wars. It’s about structural repair.

Spending needs to stabilise relative to the size of the economy. Debt reduction must extend beyond short political cycles. Government should step back from directing capital and allow private enterprise to take the lead.

In parallel, incentives need to shift - away from inflating existing land and toward funding productive businesses.

Because over time, we have tilted toward property speculation at the expense of enterprise.

That wasn’t inevitable. It was designed. And what has been designed can be redesigned.

Back to factory settings. Press reset!

A Short Break

The Matusik Missive is taking a short Easter breather.

We’ll be back on Tuesday 14 April with the next instalment. The upcoming run will focus on population growth, renovation payback/s plus market depth + direction - the structural drivers that really shape housing outcomes.

I will also update my take - as promised - of the impact of the Middle East turmoil on the Australian housing market. Well my best guess! Maybe guesses might be more apt.

And also I will return with a summary of your views on what new housing might look like in 2050.

If you haven’t yet offered your two bobs worth, this is your final call. Click on the post image below to have your say.

And have a great Easter. Try to relax. Maybe don’t watch the news. Be careful what you read and who is saying what, and why. Spend some time with those that matter. Even if it is yourself.