Internal migration reset

The big moves aren’t between states anymore - they’re within them

Synopsis

Internal migration hasn’t stopped, but it has changed shape. Capital cities are losing people, regions are gaining, and affordability is back in charge. Victoria is stabilising, Queensland is slowing, and smaller markets are adjusting. The real story is no longer where Australians move internally - but how and why they choose to do it.

A Moment with Mike

The Long Read + bonus Data Deck intel is behind paywall for paid Missive subscribers. Thanks for your brass!

The big picture

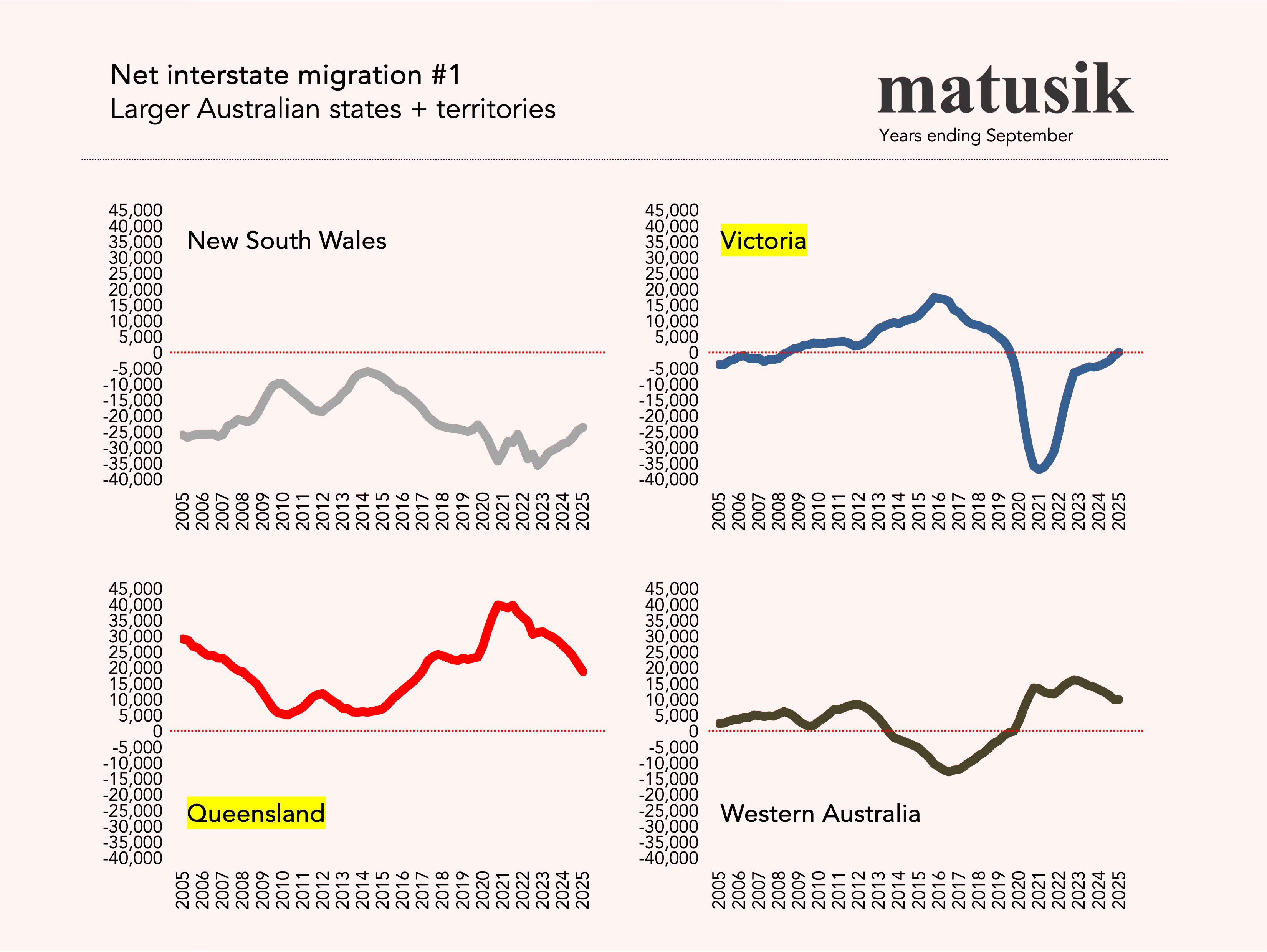

Nationally, internal migration nets to zero. It always does.

But where people are going - and leaving - tells you everything about housing markets, affordability, jobs and lifestyle trade-offs.

At a headline level:

Queensland still leads, but momentum has eased (+19,092)

Western Australia is strong (+10,272)

Victoria has quietly turned positive (+441)

New South Wales continues to bleed (-23,353)

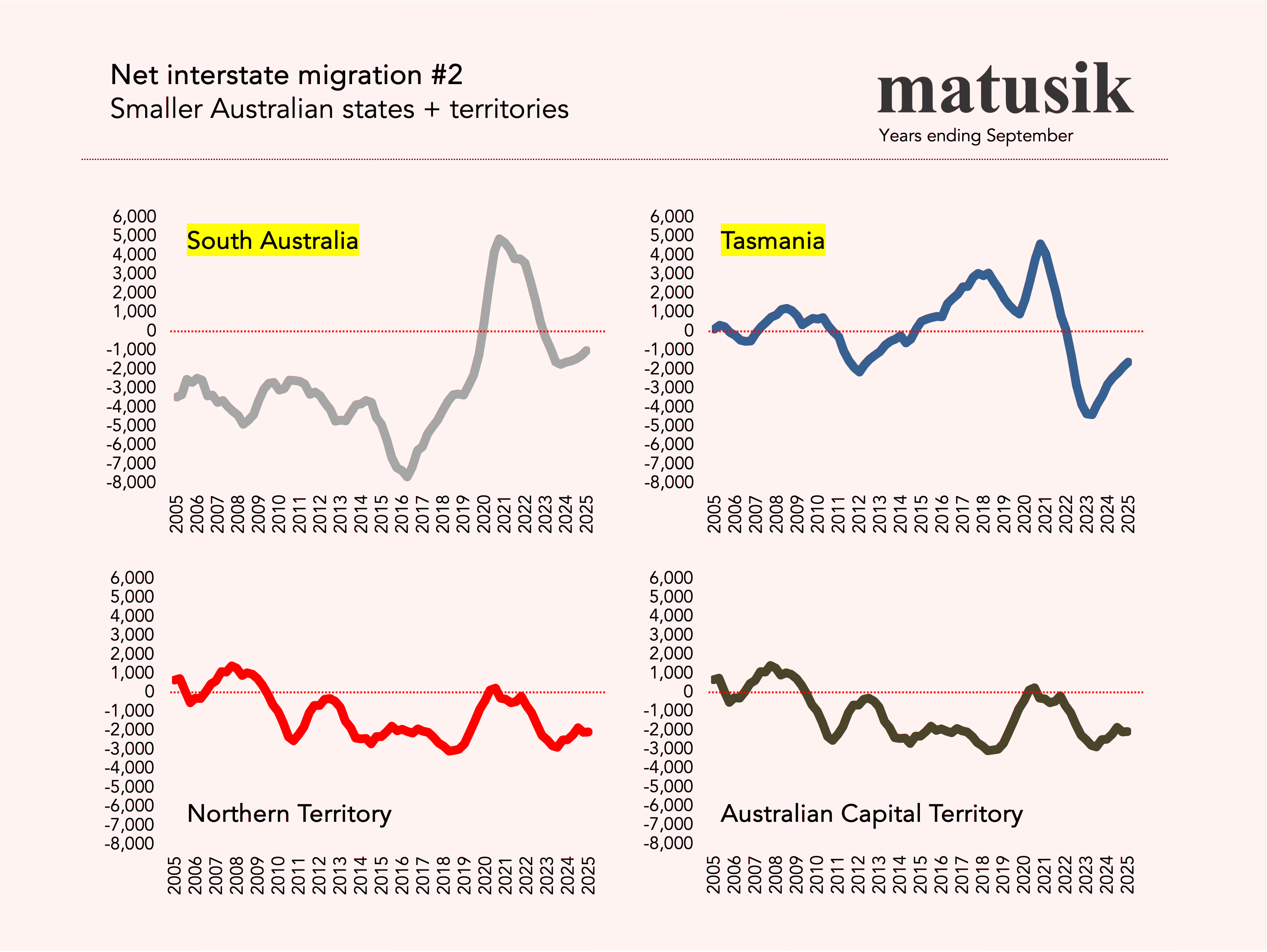

And then there are the smaller states, where the story is turning.

A big shift: cities out, regions in

Capital city population losses are being offset by equivalent gains in regional Australia, but this is not a repeat of the pandemic surge. The shift is more measured and selective.

Sydney continues to drive most capital losses, while Melbourne’s decline is modest. In contrast, Brisbane and Perth are still attracting migrants. Within regions, growth is strongest in Queensland, Victoria and New South Wales.

This is no longer a broad “move to the regions” trend. Instead, households are making more deliberate, price- and lifestyle-driven decisions, favouring affordable and opportunity-rich locations over higher-cost, established markets.

But dig deeper. Not everyone is moving:

Families and mid-lifers (45 to 64) are leading the charge

Young adults (25 to 44) are also heading out

But the 15 to 24 cohort is still city-bound

This matters. Because it tells you that migration isn’t random, it’s economic and lifecycle driven. Work, housing cost and lifestyle.

Victoria: The quiet comeback

Another surprise this post is the Victorian come back.

After years of negative headlines - government mismanagement, rising taxes, poor policy settings, falling investor sentiment - the state has posted a positive net interstate migration result.

Only just. But symbolically? It matters.

So what’s going on?

First - jobs. Victoria’s labour market has held up. Melbourne remains the largest employment hub in the country outside Sydney, and for many households, job security trumps tax settings every day of the week.

Second - relative affordability (yes, really). Not cheap. Not by a long shot. But compared to Sydney - and increasingly Brisbane - Melbourne is now looking relatively better value, especially for attached housing and small lot detached houses.

Third - normalisation. Victoria was hit hardest during COVID. It lost more people than any other state. What we are seeing now is a partial unwind of that shock. People are coming back. Not in droves. But enough to shift the dial.

And here’s the kicker - if this continues, it will place a floor under Melbourne’s housing demand, especially for well-located, mid-density and small lot housing product.

Queensland: Losing momentum

Queensland is still the dominant migration winner. But the trend is clearly softening.

From pandemic highs of 30,000–40,000+ net inflows, it is now sitting closer to 19,000.

Why? Simple. It got expensive.

The Queensland proposition used to be: Cheaper housing, better lifestyle and plenty of space.

Now? Housing costs have surged. Rents have spiked. Supply is tight - especially for new detached housing.

In short, Queensland has become a victim of its own success.

Add to that: Infrastructure lag, construction capacity constraints and Olympic-related cost pressures looming.

And the state is no longer the “easy move” it once was. It’s still attractive. But not overwhelmingly so.

South Australia: From boom to breather

South Australia has slipped back into negative net interstate migration (-1,026). Not a dramatic shift, but directionally important.

A few years ago, Adelaide was the quiet achiever: It has affordable homes, a stable economy and a very livable city.

But prices have risen sharply, and in many cases faster than incomes.

That changes behaviour. When affordability narrows, migration slows.

There’s also a smaller economic base here. Unlike Queensland or WA, there isn’t a strong population pull from large-scale job creation or major industry expansion.

So once the affordability advantage fades - the migration tailwind fades with it.

Tasmania: The hangover

Tasmania is now back to net outflows (-1,644).

Tasmania had its moment. COVID-driven relocations, lifestyle appeal and relative affordability.

But that story has run its course.

Here’s what’s biting now:

1. Jobs. The employment base simply isn’t deep enough to sustain long-term inflows, especially for younger households.

2. Housing mismatch. There isn’t enough appropriate new (and even existing) housing - particularly homes suited for the 20 to 40 age cohort.

3. Cost creep. Prices rose quickly. Wages didn’t. Far from it.

Tasmania hasn’t lost its appeal. But it has lost its edge. And a new stadium will do stuff all to correct that! The opposite, in my opinion, as monies will be foregone for the things that really matter.

My summary

This isn’t a story about one state winning and another losing. It’s about convergence.

The big pandemic-driven distortions are washing out.

Australia’s internal migration patterns are normalising around three key forces:

Relative housing costs matter most

Jobs still anchor decisions

Lifestyle is the swing factor and not the driver for most internal migrations

What this means for housing

A few takeaways worth banking:

Melbourne demand risk is easing - not gone, but stabilising

Queensland supply pressure remains, but demand growth is slowing

Smaller markets are more volatile - they rise fast, and fall faster

Regional markets are still in play, but not universally

And perhaps most importantly: There is no “one-way” internal migration story anymore.

The market is becoming more balanced. More selective. More rational.