Inflation hasn't even started yet!

Free to all + the biggest risk facing Australia right now isn't where inflation is, it's where Australians think inflation is heading.

I truly cannot comprehend how market and bank economists think that the Reserve Bank of Australia has finished with its current round of credit tightening. Some members of the dismal science are even leaning towards an easing bias in the later part of this year. I just don’t get it.

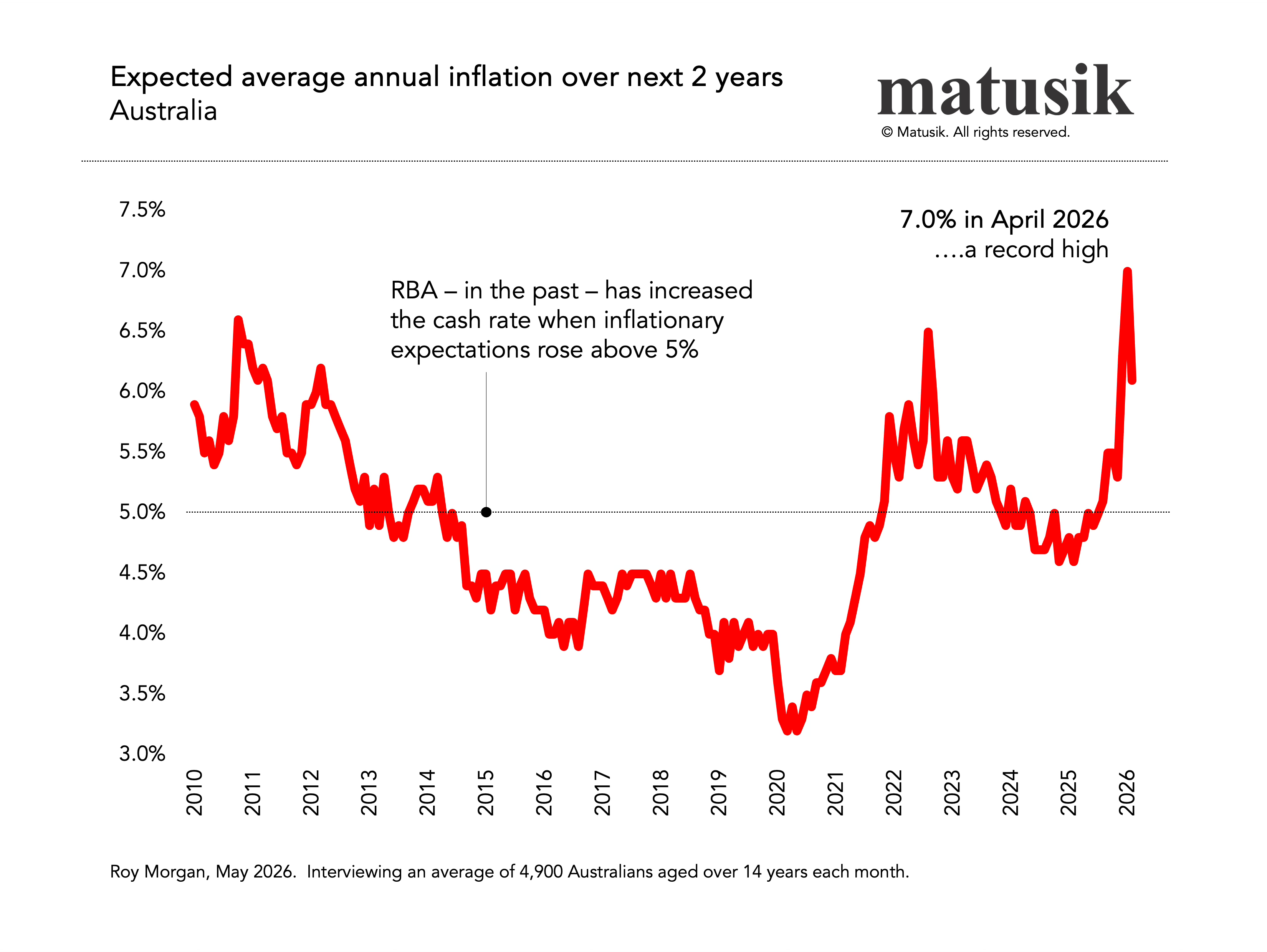

The recent ANZ-Roy Morgan Inflation Expectations survey deserves far more attention than it has received. The monthly series reported expected inflation of a whopping 7.0% for April 2026. That is the highest reading in the 16-year history of the survey. Remarkably, it sits above the levels recorded during the inflation explosion of 2022.

The chart accompanying this post tells the story.

For most of the past decade, inflation expectations generally sat between 4% and 6%. They collapsed during Covid to around 3.2%, before surging again. Now they have broken through every previous peak.

That matters.

The key issue is not simply where inflation is today. It is whether households and businesses still believe inflation will return to the RBA’s target range of 2% to 3%.

Households do not form expectations through central bank models. They form them through fuel bills, grocery receipts, rent increases, insurance renewals, electricity charges, council rates and wage negotiations.

When those costs remain visibly and persistently higher, behaviour changes.

Workers bargain more aggressively for wage increases. Businesses pre-empt future cost increases. Contracts build in larger buffers. Companies protect margins more defensively.

That is the point where inflation stops being a price problem and becomes a psychology problem. Once expectations become entrenched, restoring credibility becomes much harder and much more painful.

The fiscal backdrop isn’t helping either.

Monetary policy is trying to restrain demand while federal and state governments continue to spend, subsidise and stimulate as though inflation risk is someone else’s problem. The more fiscal policy leans against monetary restraint, the more the RBA is left carrying the burden. And that burden rarely ends well.

I think the RBA should have lifted rates in June. If inflation expectations remain elevated and underlying inflation stays above target, then further increases in August, September and November should not be ruled out.

But what concerns me even more is what comes next.

The inflationary impacts of what many are now calling Gulf War 3 have barely started to flow through the global economy.

A recent article in Foreign Affairs argued that the post-war era of relatively free global shipping is coming under increasing pressure. The article points to growing instability across critical maritime choke points including the Strait of Hormuz, the Red Sea, the Taiwan Strait and other strategic waterways.

Its central argument is simple: the world may be moving away from an era of largely unrestricted maritime trade towards one where passage becomes more contested, more expensive and more politically negotiated.

If that occurs, the implications for Australia are significant.

We are an island nation that imports much of what we consume and exports much of what we produce. Higher shipping costs, increased insurance premiums, longer supply chains and greater geopolitical risk all feed directly into prices.

For forty years, globalisation helped suppress inflation. Goods became cheaper. Supply chains became more efficient. Competition intensified.

The next decade may look very different.

If the cost of moving goods rises structurally, then inflation may prove far stickier than most economists currently expect.

That has consequences.

Higher inflation means higher interest rates. Higher interest rates mean slower economic growth. Slower growth generally means weaker asset price appreciation, including housing.

The real-world reality is that the RBA’s job is not to be popular. Its job is to preserve price stability and maintain confidence in the inflation-targeting framework.

Australia has now spent almost five years with inflation persistently above the target band. That is unacceptable.

A 7.0% inflation expectations reading should not be dismissed as noise. It should be treated as a flashing red warning light.

Because once inflation psychology breaks free from the anchor, restoring it becomes far more painful than acting before it does.

A 7.0% inflation expectations reading doesn’t exist in isolation.

Paid subscribers have spent the past few months exploring the forces sitting behind numbers like this: Gulf War 3, rising geopolitical costs, changing migration demand, hidden housing capacity, slowing asking prices, the 18-year property cycle and the growing parallels with the 1990s.

My view is that these are not separate stories. They are all part of the same economic narrative.

The paid subscription is the only place where I share that full thinking, connect the dots and publish the detailed analysis behind the headlines. If you’d like to dig deeper, you’ll find the archive waiting for you.

Financial repression.