Twice the approvals, half the demand

Why southeast Queensland’s housing pipeline is structurally misaligned

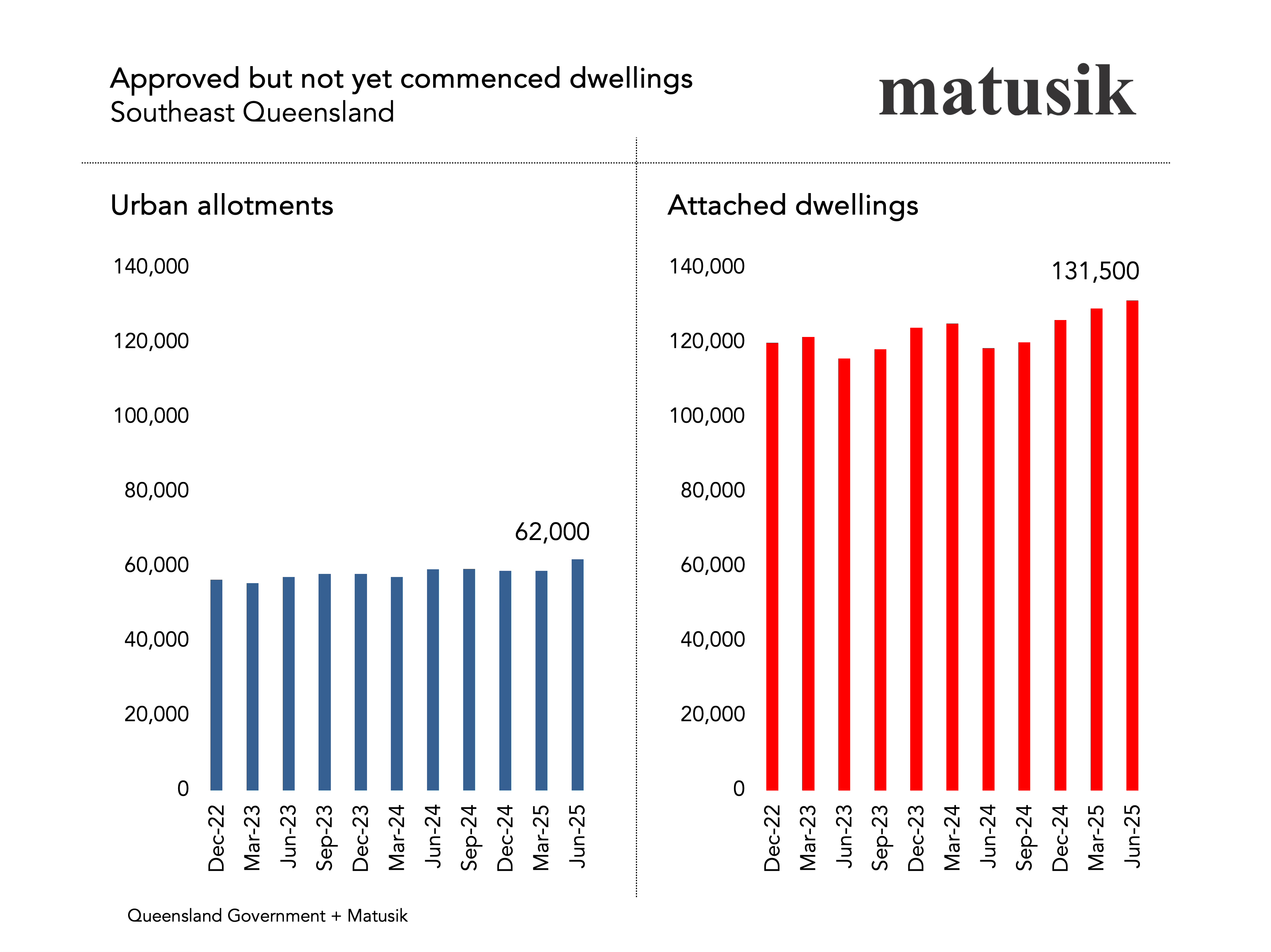

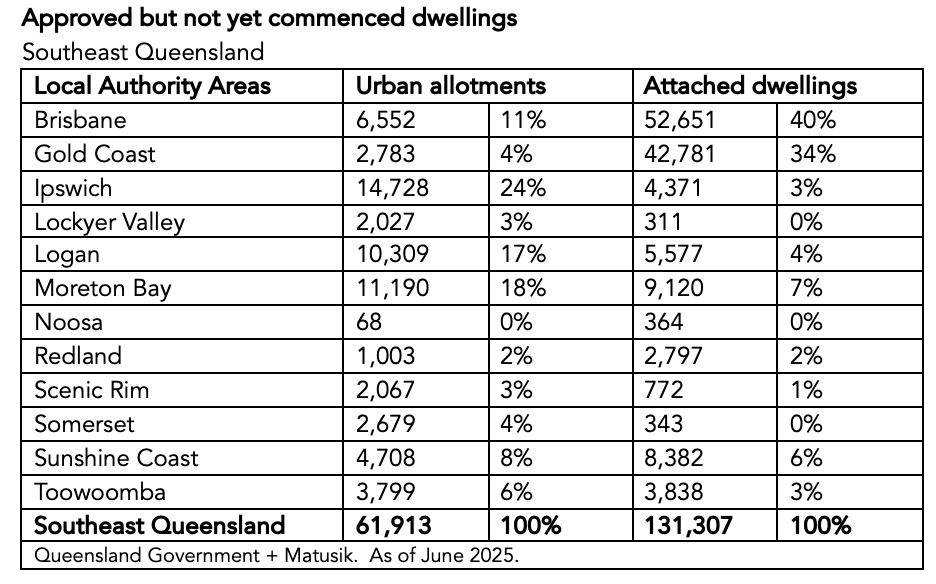

As at June 2025 there are 61,913 approved but not yet commenced urban allotments across Southeast Queensland, compared with 131,307 approved attached dwellings. In simple terms, there is more than twice as much approved stock sitting in the attached sector.

Now consider demand

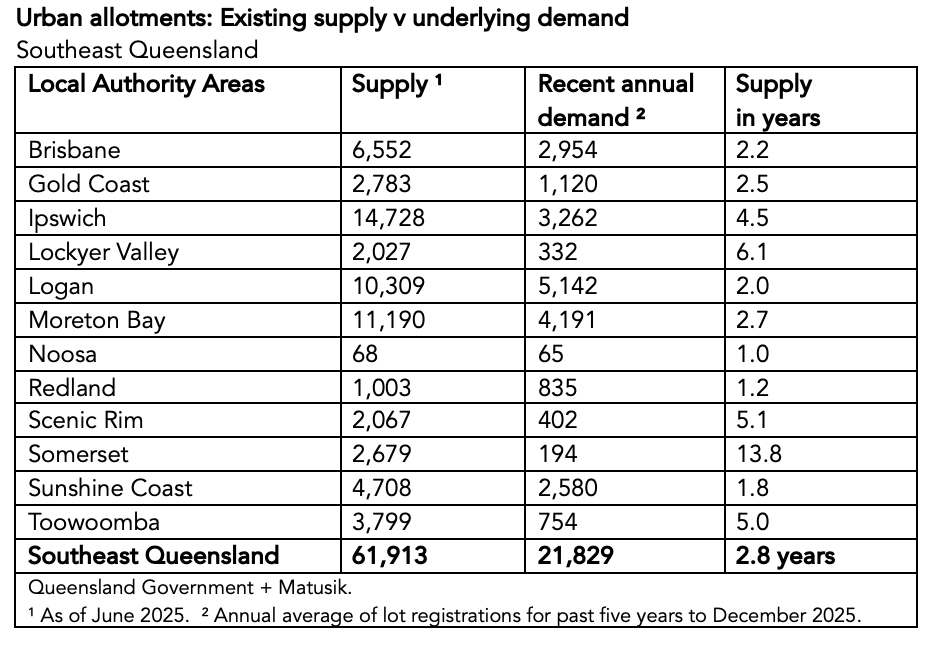

Detached housing is currently absorbing around 21,829 lots per annum across the region, which is roughly 22,000 commencements a year. That equates to just 2.8 years of supply regionally based on the 62,000 potential supply count.

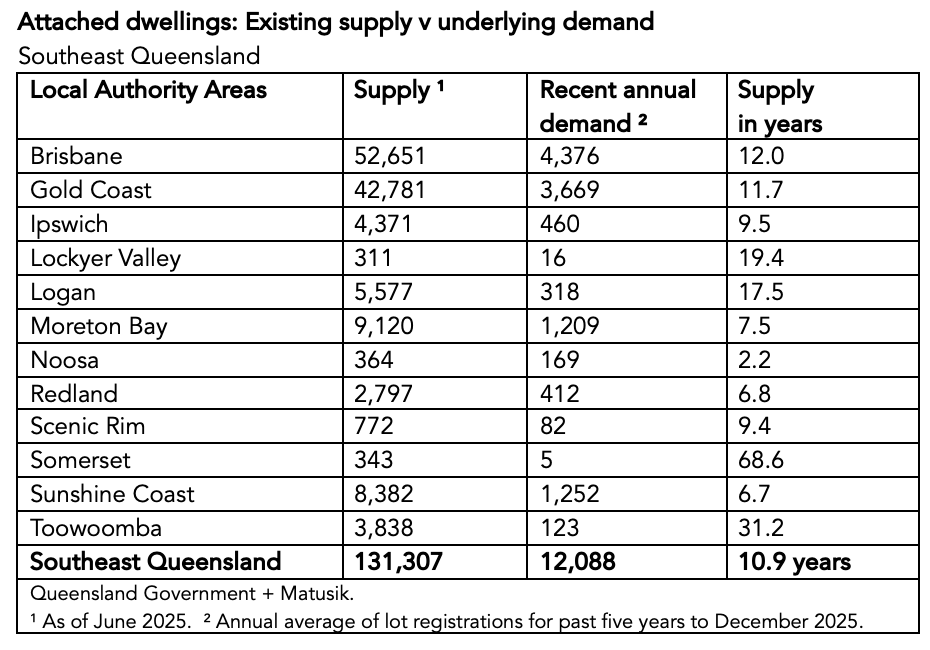

Attached product is running at about 12,088 dwellings per annum in underlying demand, leaving 10.9 years of approved supply sitting in the system.

The mismatch is obvious

Brisbane and the Gold Coast alone account for close to three quarters of attached approvals, with more than a decade of supply at current absorption rates. Meanwhile, detached supply is tightest in Brisbane, Logan, the Sunshine Coast and Redland, generally sitting under three years.

If we are serious about aligning supply with demand, two things stand out.

First, something needs to unlock the attached backlog. That could be feasibility settings, funding constraints, infrastructure timing or staging. Whatever the handbrake is, it needs attention.

Second, we need to be more deliberate about accelerating detached commencements west of Brisbane, particularly in Ipswich, Lockyer Valley, Somerset and the Scenic Rim, where land exists and supply buffers are more workable.

Approvals are not the issue. Conversion is.

Revisit