A viscous cycle

How housing policy, inflation and the RBA are now tightly intertwined

Synopsis

Housing makes up over 20% of CPI, and it’s running hotter than headline inflation. Since October’s expanded 5% Deposit Scheme, lower-quartile home values have surged across most capitals. Demand worked. Prices lifted. Housing inflation strengthened. And when housing inflation rises, the RBA notices and reacts.

A dilemma

There seems to be ongoing confusion about the role housing is playing in Australian inflation and whether the recently expanded 5% Deposit Scheme has anything to do with the current CPI pulse and the February 2026 official interest rate lift.

Let’s start with the facts.

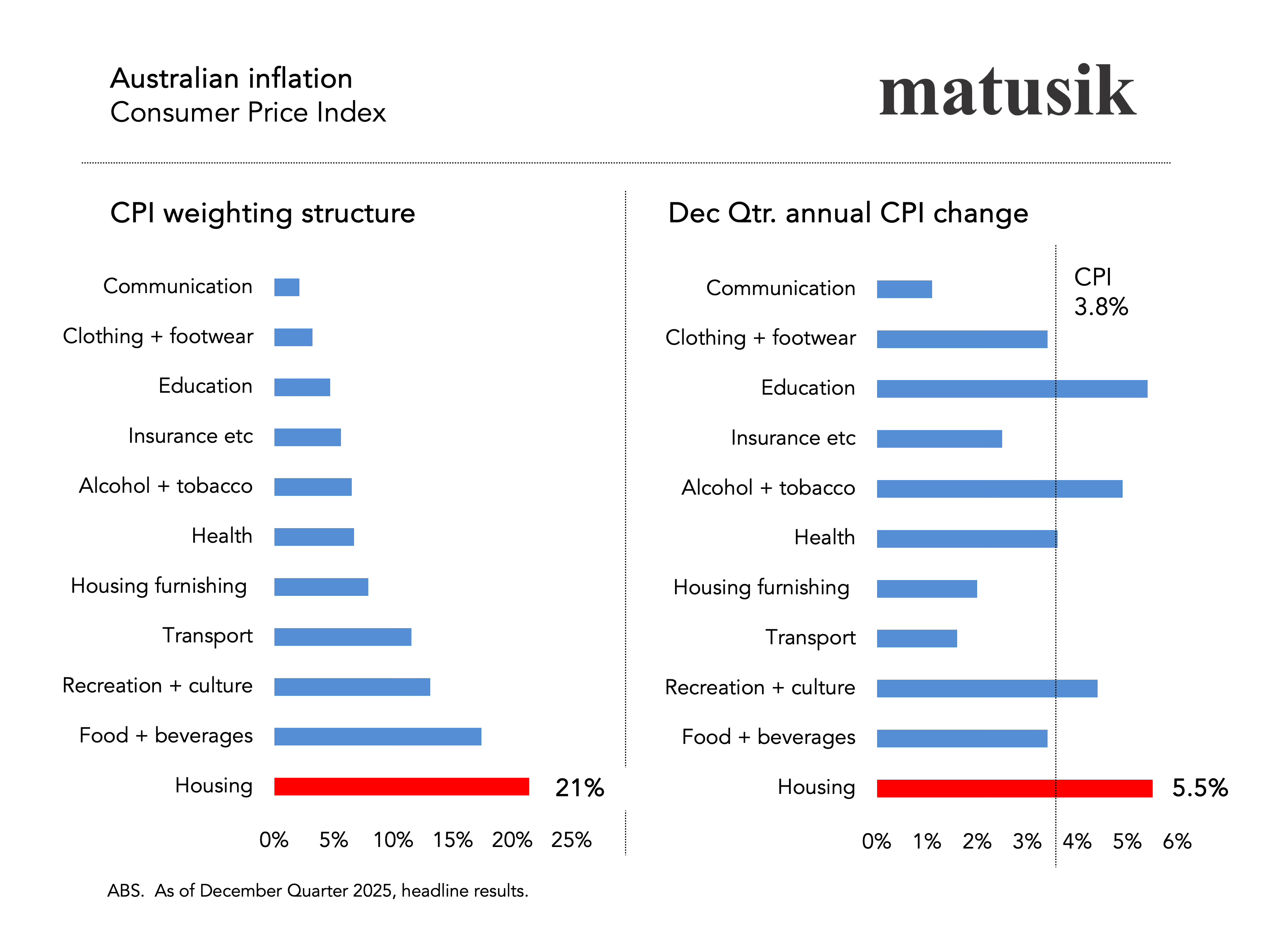

Housing carries roughly 21–23% of the CPI basket. Within that, rents account for about 7–8% of total CPI, while new dwelling purchases sit at roughly 8–9%. In other words, rents and new housing construction make up close to 80% of the housing component.

So when housing moves, inflation moves.

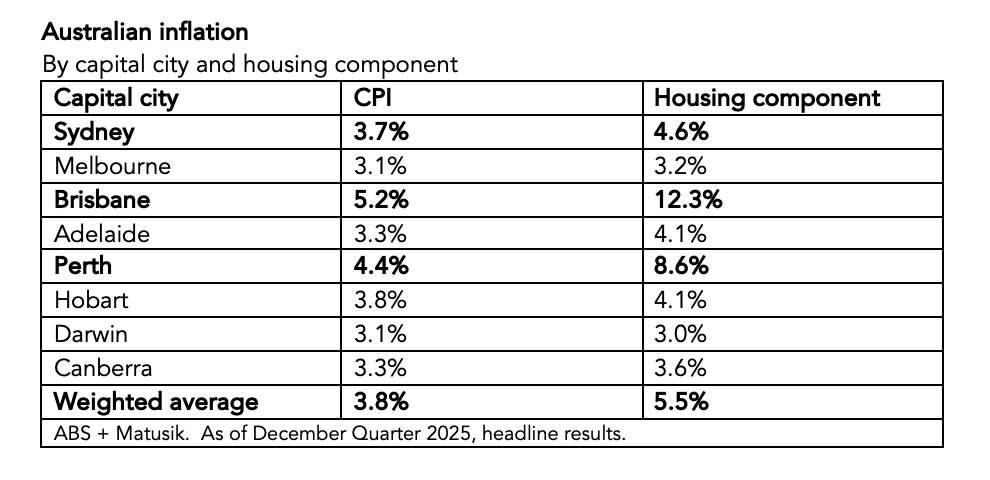

The latest December quarter data shows a weighted average CPI of 3.8%, but the housing component - as shown in the chart above - is running hotter at 5.5%

Look closer and the divergence is stark.

The table shows that Brisbane CPI is 5.2%, but housing inflation is running at 12.3%.

Perth CPI is 4.4%, housing 8.6%. Sydney CPI 3.7%, housing 4.6%.

Housing is not a sideshow. It’s driving the bus.

Now overlay what happened from October 2025.

The expanded 5% Deposit Scheme removed caps and widened eligibility. In October alone, 5,778 homes were purchased using the scheme - roughly one in ten transactions nationwide. Applications reportedly doubled at major lenders. First-home buyer loans rose 6.8% in the December quarter to just under 32,000. Housing finance overall lifted 5.1%. Investors were up 5.5%. But investors are mostly buying resale stock not new digs.

Revisit

The deposit scheme is working in the narrow sense it was designed to. But demand-side stimulus in a supply-constrained market has its consequences.

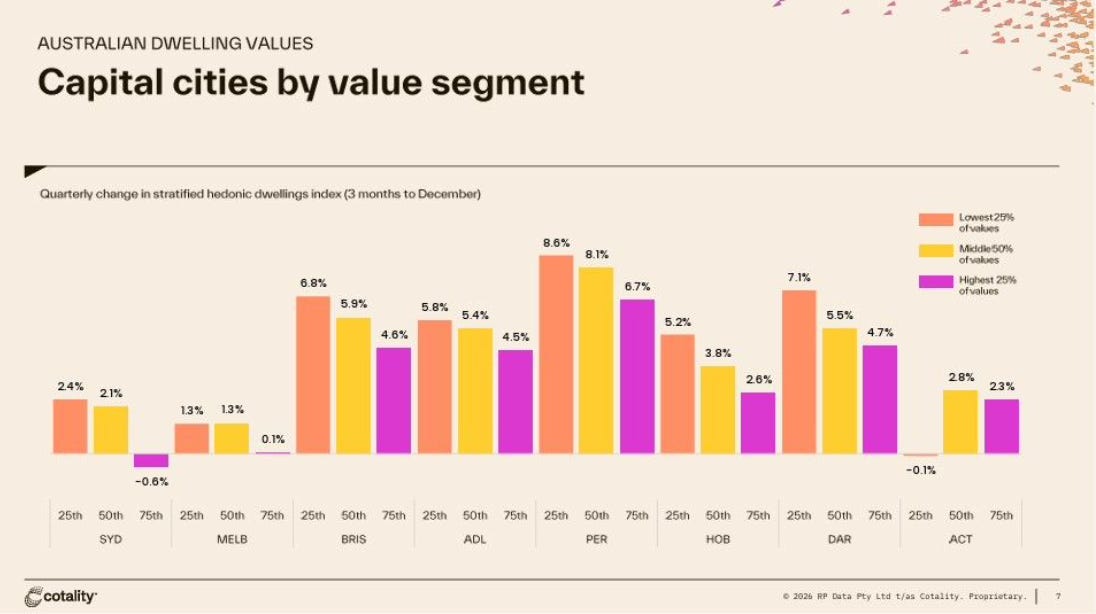

The recent Cotality chart tells the story. Over the past three months, in almost every capital city bar Canberra, the lowest value quartile recorded the strongest growth, while the top end recorded the weakest. That’s textbook first-home-buyer stimulus impact.

Economical housing stock has become less affordable and this feeds directly into CPI via two channels.

First, stronger prices at the lower end (and often across the middle market segment too) eventually reset rental benchmarks.

Second, elevated new-dwelling demand sustains construction costs, which sit squarely inside CPI.

Blame game

Did the 5% scheme single-handedly cause the February rate rise? Of course not.

But did it contribute to the demand impulse that is now showing up in both dwelling values and the housing CPI component? It would be naïve to suggest otherwise.

Since 2020, over 248,000 Australians have used the federal deposit guarantee schemes. I’ll unpack the longer trend and its impact in my next missive. For now, focus on the current expansion and its immediate market impact.

Governments want higher home ownership without lower house prices. I understand the politics.

But here’s the economic tension: if the lowest quartile keeps lifting faster than incomes, future first-home buyers will require even more assistance - and take on more debt - to enter the market.

Accessibility improves. Affordability stretches. CPI absorbs it. The RBA responds.

And around we go. A viscous cycle indeed.

Until supply expands meaningfully, injecting demand into housing will keep doing what it has always done. Push housing prices higher and inflation with it.

And as a result another rate rise - maybe two - is almost baked in for this year.