A can of worms

Last week’s post triggered quite a few questions

Well last week’s post opened a can of worms.

So, in coming weeks I will tackle some of the issues raised.

This week let’s look a supply and demand.

Detached houses

My first chart this post shows that there are some 165,300 residential allotments currently approved and possible over the next decade across southeast Queensland. Half of this supply is in Logan and Ipswich.

Of the approved land supply, some 45% of 60,000 allotments currently have operational works. So, they can be – in theory - built subject to economical labour and material supplies.

Future supply – between 2026 and 2036 – amounts to 106,000 allotments, across 12,580 hectares. So, delivery is expected to be around 8.4 dwellings per hectare. This includes rural dwellings.

When looking at the just urban land solutions the anticipated yield rises to 10 dwellings per hectare, which as outlined last week, is way too low if you ask me. The target should be closer to between 15 and 18.

Importantly the new potential detached housing supply does not consider ownership, fragmentation, planning constraints, and owner price expectations, so the actual delivery is likely to be less than the 106,000 new lots over the next decade.

My workings suggest that there is likely to be a need to build some 18,000 new detached homes across southeast Queensland, each year, between now and 2036.

Even when counting all approved and potential allotments, there is just 9 years’ worth of supply. But if past development delivery rates continue, then the supply drops by half, to 4.5 years.

Something needs to be done here and fast.

Apartments (and townhouses)

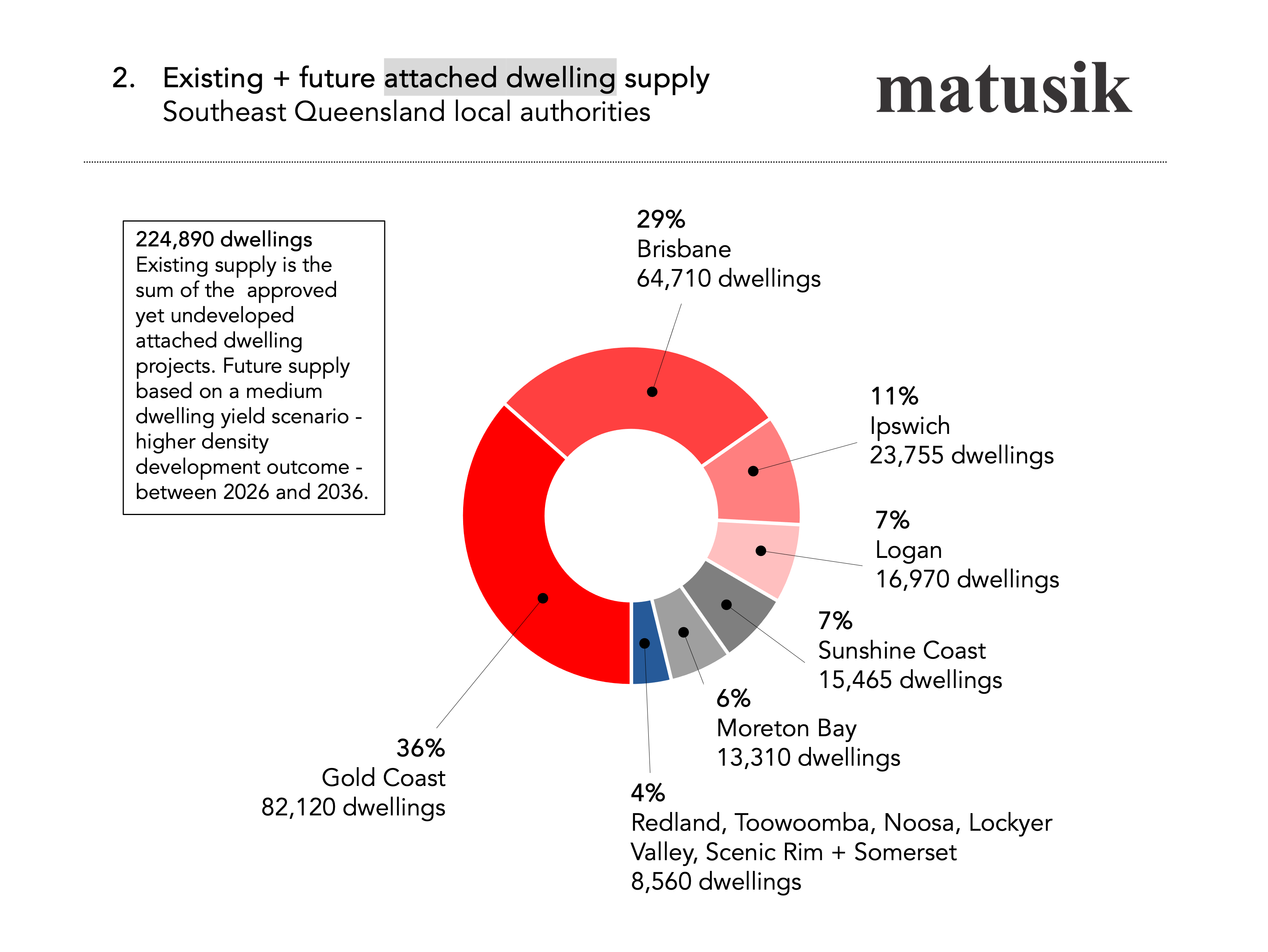

The second chart shows that existing and potential attached dwelling supply (also over the next decade) is close to 225,000 dwellings. The Gold Coast and Brisbane are expected to deliver the lion’s share.

Future supply – between 2026 and 2036 – amounts to 102,000 dwellings, across 1,640 hectares. So, when it comes to attached dwelling delivery, the expected yield averages 62 dwellings per hectare.

This yield – in contrast to the detached housing supply – is way too high.

The Gold Coast’s target is an eyewatering 115 dwellings per hectare. Brisbane’s is 91 and Ipswich’s 77! The Sunshine Coast, Moreton Bay and Logan have more realistic future yields ranging between 29 and 32 dwellings per hectare.

By way of comparison, there are just 15 suburbs across Australia with a housing density higher than 110 dwellings per hectare, twelve of which are in inner Sydney and three are in Melbourne.

Kangaroo Point is the ‘densest’ suburb in Queensland at 88 dwellings per hectare. Surfers Paradise holds 51 dwellings per hectare.

So, the anticipated outcome for southeast Queensland, is that there will be more attached dwellings (mostly apartments) with 60% of the new housing supply over the next decade and that these new digs will be delivered at a density higher than that achieved across Surfers Paradise.

And the Gold Coast will deliver new homes at twice the density of its most crowded suburb. Nuts!

My workings suggest that there should be a need to build some 16,500 new attached dwellings homes across southeast Queensland, each year, between now and 2036. This is about 1,500 less than the annual detached house demand over the same time.

There is a demand for new apartments and townhouses, but at the right price and in the appropriate density configurations.

When counting all approved and potential attached dwelling, there is 14 years’ worth of attached housing supply. But if past development delivery rates continue, then the likely supply drops to under eight (8) years.

A massive rethink is needed here too.

Last week’s post. Paid subscribers get access to the Long Read plus 12 charts outlining in detail what is going on across the southeast Queensland new housing market.

Paid subscribers also get the information covered in this post for all 12 SEQld LGA’s.

Go below the paywall to access. To become a paid sub – and thanks if you do – click on red blob below for more information and payment gateway.

Six tables outlining the supply and demand status for all 12 LGAs across SEQld follows: